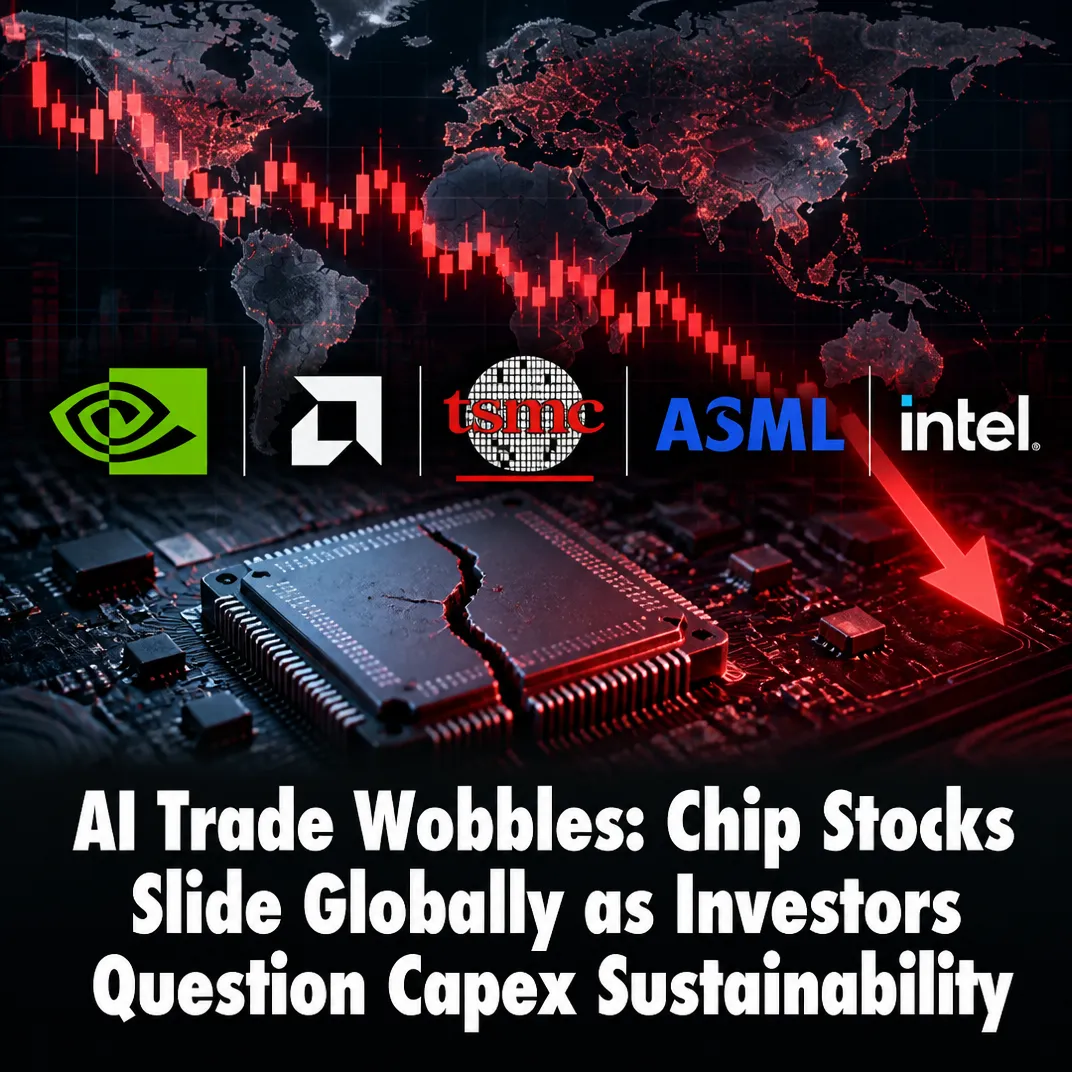

July 17, 2026, (Inside AI) — A sharp rotation out of high-flying semiconductor and technology stocks accelerated this week, pushing the Philadelphia SE Semiconductor Index toward its steepest weekly decline in over a year. The index has fallen 11% this week, leaving it down nearly 24% from its late June all-time high and on the cusp of confirming a bear market.

The sell-off rippled from Seoul to Europe, dragging down AI-exposed names that had dominated portfolio returns. Nvidia lost 3%, while Qualcomm and Broadcom each shed about 2%. Memory chip favorites Micron and SanDisk fell roughly 3% each. SK Hynix's U.S.-listed shares dropped 2.7%, trading near their offering price and down more than 9% this week.

The pullback reflects a confluence of profit-taking, stretched valuations, and rising skepticism about the pace of returns from massive AI capital expenditures. "The pullback reflects profit-taking and rising scrutiny of AI capex sustainability," said Toni Meadows, head of investment at BRI Wealth Management.

"Valuations in semiconductor stocks had priced near-perfect demand, for what has been a cyclical area in the past, so was always going to leave stocks vulnerable at some point in what has been a rapid rise."

The chip index had surged nearly 62% for the year as of early Friday trading, but analysts point to specific catalysts that punctured the exuberance. Chinese AI startup Moonshot unveiled Kimi K3, a 2.8 trillion-parameter model it claims is the world's largest open-weight AI system. The announcement rekindled investor concerns that U.S. tech firms' heavy AI investments may face diminishing returns or intensified global competition.

Adding to the unease, a report on Thursday indicated that Alphabet's Google is months behind schedule on releasing Gemini 3.5 Pro, its most powerful flagship AI model. The delay suggests that even well-resourced tech giants are encountering hurdles in scaling frontier models, potentially slowing the revenue streams investors have banked on.

Strong forecasts from TSMC, the world's largest chip manufacturer, and European semiconductor equipment maker ASML failed to halt the slide. This signals that the market is now questioning the broader AI trade rather than reacting to single-company fundamentals. The rotation has been brutal for momentum-driven strategies: the S&P 500 Momentum Index has pulled back 10% in July, compared to just a 0.8% dip in the broader market.

Global markets have had a volatile July. South Korea's KOSPI index confirmed a bear market last week, even as it remains up nearly 70% for the year. Japan's Nikkei tumbled into correction territory on Friday. Europe's tech sector is among the top losers this week, after notching its biggest quarterly jump since 2001 in June.

Space-related stocks, which had rallied in anticipation of SpaceX's debut, also suffered. SpaceX lost 4% after a last-second abort of Starship's 13th flight test, adding pressure after the stock slipped below its $135 per share IPO price earlier this week. Rocket Lab and Intuitive Machines were down 3% and 4% on Friday, respectively, on track for weekly losses of about 20% each.

The focus now shifts to earnings reports from two of Wall Street's "Magnificent Seven"—Alphabet and Tesla—scheduled for next week. Their results and guidance will be closely parsed for signs of whether AI spending is translating into tangible financial results, or if the recent pullback is the start of a deeper reckoning for the AI trade.