Critics and boosters are both looking in the wrong place

By Arvind Narayanan and Akash Kapur

Our goal in this essay is to move beyond the debate over whether AI is a bubble. We do so in two ways: clearly separating current financials from the question of who captures value in the long run, and recognizing that the labs are not confined to be model providers. They can migrate up the stack and are already aggressively doing so. This will likely allow them to escape the commodity trap but raises new concerns — customer lock-in and reduced competition.

Akash Kapur is a visiting fellow at Princeton and a senior fellow at New America. He is no relation to Sayash Kapoor.

As leading AI companies continue to invest massively in capacity and race toward blockbuster IPOs, serious questions linger about their business models. How will these companies — along with the vast ecosystem of chipmakers, hyperscalers, and infrastructure partners that depends on them — recoup the estimated $4–8 trillion projected to be invested in AI infrastructure by the early 2030s?

The current conversation splits between critics and boosters. Critics point to mounting losses, the gap between capex and revenue, and reports about the leading labs’ massive cash burn. Boosters cite accelerating rapid revenue growth, enterprise adoption, and milestones like Anthropic’s first profitable quarter. Each camp has a valid point. But both are looking in the wrong place — the same quarterly statements, the same short-term view of an industry that remains in flux.

In recent months, we have been thinking about the nature and sustainability of the AI business, and we’ve landed in a different place than most of the existing commentary. AI companies today earn much of their revenue by charging for inference, but the conditions of frontier inference make this an unusually difficult business to maintain. Models are largely undifferentiated, the leading labs operate with similar capital structures, switching costs are low, and prices can be adjusted freely. All of this appears to set up the conditions for a commodity trap that would pose real challenges to the task of building high-margin or even profitable businesses.

At the same time, we believe that the industry remains in a transitional stage, and that its structure will look very different when it matures. Drawing on both historical evidence and economic theory, we argue that competition in this equilibrium is likely to push the price of model inference toward the marginal cost of producing tokens, leaving little room for durable profits at the model layer. This does not mean, however, that the business of AI is inherently unviable. The same analysis suggests a path forward for AI labs, and leads to the central argument of our paper:

The labs’ most likely path to durable profitability runs not through the foundation layers (chips, datacenters, models) that have thus far accounted for the bulk of investments, but higher up the stack, through a mix of vertical integration, embedded enterprise deployments, and the deliberate construction of switching costs and other “moats”.

The labs’ strategies to capture value by moving up the stack, many borrowed from the playbook of enterprise software, have already begun. Beyond the sustainability of the current AI ecosystem, they raise questions of broader societal concern — about competition, innovation, and the overall distribution of economic and political power. The public discussion over AI so far has been marked by a somewhat paradoxical dichotomy: anxiety about monopolistic concentration and runaway market power, yet a reality of low switching costs and relatively interchangeable models that seems to belie those fears. But if we are right that the labs will increasingly move higher up the stack, then concerns about concentration and competition are worth taking seriously now, rather than after the effects of lock-in start to materialize. We return to these broader issues in the conclusion — and in a forthcoming paper that dives deeper into many of the topics covered in this post.

Historical analysis: the infrastructure layer overwhelmingly fails to capture the value that it creates

The * AI as Normal Technology* framework is committed to drawing lessons, when applicable, from past transformative technologies. We think AI is subject to many of the same dynamics related to investment, competition, and value capture that have shaped previous waves of technological innovation. As part of our research, we therefore examined the puzzle of AI value capture, and the labs’ likely response to it, through a broader historical lens.

We looked at six historical instances of capital-intensive infrastructure industries (railroads, electricity, telecom and fiber, cloud computing, semiconductor manufacturing, and commercial aviation). We believe that AI today has many infrastructure-like characteristics: massive capital requirements; low marginal cost; a commodity product that is somewhat decoupled from the applications that ultimately create value. This makes infrastructure a notoriously tough business to be in.

But at the same time, AI is software, and the software business has historically been lucrative, with exceptionally high margins. The industry has software-margin ambitions. Thus, we also surveyed the value-add and lock-in strategies of software-as-a-service, and analyzed whether AI can replicate these. Our thesis is that AI companies’ sustainability and value-capture largely turns on how successfully they can migrate from the first set of infrastructural properties toward the second enterprise-software ones.

Broadly, we identified three instructive lessons for AI from our historical analysis. First, infrastructure providers rarely capture the value they create. Across railroads, electricity, telecom, and airlines, the firms that built capacity were eventually competed, regulated, or commoditized into thin margins. In many cases, they were destroyed outright. During the telecom and fiber buildout of the late 1990s, capacity exploded 186,000-fold in seven years, prices crashed, and roughly $2 trillion in market capitalization was erased. The value generated by the infrastructure primarily accrued to industries and applications built on top of it. Commercial aviation has destroyed investor capital for eight decades, because typical net margins are 2–4%, often below the cost of capital — even as businesses of all stripes benefited from a globalized economy.

We believe that AI, at least in its current hyperscaler form, risks falling into the same commodity trap that has bedeviled so many previous infrastructure builders. Carlota Perez has theorized the paradoxical phenomenon that the builders who create infrastructure during the “installation period” rarely survive to capture the value it creates.

Second, enterprise software is not subject to this pattern, and it escapes the trap through a specific and reproducible set of mechanisms. Where infrastructure firms have struggled, enterprise software has sustained gross margins of 75% or more for decades. It does so by combining three properties that infrastructure businesses lack: zero marginal cost of reproduction, deep switching costs, and non-ephemeral value that allows fixed buildout costs to be amortized over decades. The AI labs’ lock-in strategies are best understood as attempts to import these structural properties of software into AI.

Finally, two partial exceptions reveal what it may take for AI to beat the historical odds. Two infrastructure businesses — cloud computing and chip fabrication — have managed to escape the commodity trap. Cloud acquired software-like properties (managed-services lock-in, egress fees, committed-spend agreements) and TSMC achieved a near-monopoly position in leading-edge fabrication. These cases matter because they show what escape from the commodity trap actually requires. Capital-intensive industries can sustain durable margins, but only by either becoming functionally software or achieving market concentration.

Why we think charging for model inference won’t allow recouping infrastructure investment

As noted, critics of the AI buildout point to the labs’ current losses and boosters to early profits, but both are committing the same error: mistaking the transitional period for the equilibrium. We are still in the early years of the AI transformation of the economy, and naive extrapolation is flawed. In equilibrium, both the supply and demand side will look very different than they do today.

A few examples of the fluctuating fortunes of the AI labs so far: A massive and speculative infrastructure buildout that was arguably ahead of demand; the Deepseek moment during which open-weight models almost caught up to the frontier; a surge in demand as companies embraced AI agents, often accompanied by irrational and wasteful practices such as token leaderboards, leading to a so-called era of token scarcity; and, most recently, a renewed push for a competitive open-source ecosystem as companies reconsider their spending on frontier models.

These ups and downs have many parallels in the historical case studies mentioned above. The railways at first saw a speculative frenzy (the railway mania of the 1840s in Britain). In America, over time, demand exceeded capacity, resulting in estimated direct and indirect returns of 15% per annum on railroad capital through 1860 — enormous for the era. But as the network matured, capacity caught up to demand, competition squeezed margins, and many railroad companies went bankrupt.

Thus, to better forecast the labs’ long-term prospects, it is helpful to step back from the year-to-year and quarter-to-quarter swings in financials (and narratives), and ground our analysis in economic theory. A key concept is the Bertrand paradox: this says that when firms sell a homogeneous product (frontier-model inference), price competition will force them to sell each unit (token) at the marginal cost of producing it.

The theoretical analysis is important because the question of how well the historical record predicts the AI industry’s fortunes is contested. For example, our colleague Mihir Kshirsagar identifies regulation as the main reason why railroad, electric and telecom companies were unable to extract the surplus generated by their infrastructure, rather than viewing it as an inherent consequence of their economics. Thus, the theory gives us an additional reason to expect a margin squeeze. Although the theoretical paradox is easy to escape in practice, we believe that model inference contains an unusually pure version of the conditions that produce the paradox:

Models are largely undifferentiated. At least three companies, OpenAI, Anthropic, and Google have managed to stay on the frontier and produce models that behave and perform similarly to each other. Besides, for an increasing fraction of use cases, frontier performance is not necessary, and open-weight models aregood enough. Furthermore, the near-equivalence of models is readily observed or perceived by customers, because there are hundreds of benchmarks on which models are regularly evaluated and frontier models all tend to cluster near the top.

For a revealing contrast from another industry, Apple famously sustains high margins by escaping this aspect of Bertrand competition. It resists competing on objectively observable dimensions of performance (gigahertz, megapixels), instead advertising outcomes and ineffable qualities (“it just works”) and creates strong brand differentiation.The vendors all have similar capital costs. AI knowledge diffuses rapidly; the major paradigms of model development — model scaling, inference scaling, reinforcement learning, and so on — have all proceeded in near-lockstep. So to produce a token at a given output quality, the labs all spend similar amounts on training. In a hypothetical future where the frontier doesn’t move as rapidly, costs will be dominated by inference, and inference cost tends to be even more similar than training cost.*Lack of geographic differentiation.*In the case of the railroads, a patchwork of local monopolies, and captive capacity, provided some defense against margin compression. The business of AI inference lacks this differentiation, and firms can effectively serve the full market. While there is arguably a token capacity constraint today, we expect this to be temporary.Prices can be changed freely, with no collusion. Railroads and utilities were able to collude tacitly or explicitly to keep prices high at some points in their history. But this is highly unlikely with AI models because there is fierce competition from sub-frontier models.*Switching costs are minimal.*Even the friction of migrating APIs is largely eliminated by a layer of provider-agnosticroutingtools.1 One potential response to all this is to argue that it doesn’t matter how much margins get squeezed, because AI companies will simply make it up in volume. But the numbers don’t work out. If we assume a 5% net margin — much higher than airlines — and the need to recoup the aforementioned $4T — $8T of investment over a 5-year horizon, we end up with a requirement of $16 – $32T in annual revenue, the higher end of which is a quarter of today’s world GDP.

Taking this longer-term perspective, grounded in history and economic theory, allows us to ignore several factors that other analysts tend to critically index on. For now, we are in a period in which massive, capital-intensive training runs continue to produce better models. This forces labs to stay on an upgrade treadmill in which they reinvest their revenues into training (and then some) taking on ever-higher investments. When this treadmill slows,2 the business will reach a new stage of equilibrium that is likely to look very different from today. In that state, three factors that currently dominate the debate will matter far less than they appear to now.

The first is falling token prices driven by efficiency improvements, which critics cite as evidence of a race to the bottom that will shrink the size of the pie. In our view, while it is true that token prices have been falling rapidly (and that this trend will likely continue), it is not necessarily a problem for the labs. Depending on the shape of the demand curve, unlocking demand could more than compensate for falling prices — the so-called Jevons’ paradox, in which efficiency gains lead to greater (not less) consumption of a resource.

The second is token scarcity, which boosters cite as evidence of the labs’ pricing power. Any scarcity, however, is likely a temporary phenomenon that will be alleviated or eliminated by a combination of infrastructure investment and algorithmic improvements. Token scarcity is therefore unlikely to allow the labs to increase their margins.

The third factor that dominates the current discourse is willingness to pay. Critics sometimes predict that demand will evaporate when labs end their subsidized, below-cost subscription pricing. But this treats willingness to pay as a fixed quantity, something that can be extrapolated forward from today. Over the long run, we expect that AI will be an essential part of most knowledge work, and that the technology will be as transformative as the industrial revolution. In a transition of this scale, the willingness to pay is potentially enormous.

In other words, we must distinguish between value creation and value capture. We expect the value created to be unfathomably large. The central — perhaps even existential — question for the labs is whether they will be able to capture even a small percentage of that value. What fraction of the value AI creates for a company will that company be willing to pay the AI vendors? This is not some free-floating, exogenously determined number. It is largely determined by the extent to which AI labs are able to escape the commodity trap.

As we argue below, the most reliable way to escape the commodity trap is to move downstream in the economic value chain (in the case of AI, this means moving “up the stack”). Transitioning from selling physical infrastructure or products to bundles that include services is sometimes called “servitization”. For example, as hardware became commoditized, IBM successfully transitioned to a services company, eventually selling its PC division altogether to Lenovo. The telecom companies also made sustained, strenuous efforts to avoid becoming “dumb pipes”, but unsuccessfully. Value was instead captured by applications that utilized the infrastructure, leading to the rise of Big Tech. We believe that labs now face much the same fork: capture value in the layers above the models, or watch others create lucrative businesses on top of the infrastructure they built and paid for.

How the labs are responding

To summarize our argument so far, our historical analysis as well as economic theory suggests that there exist only two plausible routes out of the commodity trap: establishing monopoly-like control over the market, or capturing value at higher layers of the stack, often accompanied by increased switching costs.

We believe that the first route is unlikely and the frontier will stay competitive. Proponents of AI exceptionalism might disagree, forecasting a development without historical precedent: a capability discontinuity so dramatic that it reshapes the competitive landscape entirely. In this “hard takeoff” scenario, one or more labs achieves recursive self-improvement, rendering the current economics largely irrelevant.

In our full paper, we argue why this scenario is highly implausible. For now, we point out that many policymakers, investors, and other stakeholders are not comfortable betting on such a possibility, and must instead plan for a scenario where it doesn’t pan out.

This leaves moving up the stack as the most likely path forward. We believe AI companies are well aware of the commodity trap; they are full-throatedly transitioning beyond being pure inference vendors (i.e., selling undifferentiated tokens through model APIs), and seeking to pursue value capture at higher layers of the stack. We are in the early days of these efforts and many new and more systematic strategies are likely to emerge (we examine some in the next section). But already, some efforts are apparent.

Products like ChatGPT or Claude Code sit at a layer above models. Products are not interchangeable in the way models are, for a host of technical, contractual, and behavioral reasons, as we discuss in the following section. In OpenAI’s case, ChatGPT, not the OpenAI API, has long accounted for the majority of its

revenues. Anthropic’s revenues in early 2026 were still dominated by its API, but with theexplosive growthof Claude Code, that might not last for much longer.The next layer in the stack is AI-native SaaS or “intelligence as a service”, and the labs have made early moves in this direction: ChatGPT’s

company knowledgefeature, and Anthropic’s vision ofagents inside the System of Record. However, this is the layer where the labs are most vulnerable to existing SaaS incumbents,notably Microsoft.AI companies are also pursuing bespoke deployment and workflow redesign — through

forward-deployed engineersandpartnershipswith consulting companies. This doesn’t fit cleanly into the stack. The stack assumes an equilibrium in which workplaces have been transformed through AI, whereas this category is about attempting to monetize the transformation itself.The most speculative, and more potentially lucrative, avenue for value capture is the top layer of the stack: the idea of AI agents as “digital workers”. Many companies have been

toutingthisidea. Perhaps the first release from a major AI company that has beendesignedto function analogously to a digital worker rather than a tool isClaude Tag, launched in June 2026. A digital worker that is embedded with every team in a company quickly becomes a store of tacit knowledge for the whole organization and becomes essential to workflows and business processes across different teams. Unless portability is explicitly built in, it becomes a digital employee that effectively cannot be fired, creating a level of lock-in that exceeds that of enterprise software at its worst. When companies sell digital workers, the total addressable market is the economy’s entire labor spend, far larger than companies’ IT budgets. But precisely for these reasons, the vision is likely to encounter the most resistance from enterprises.

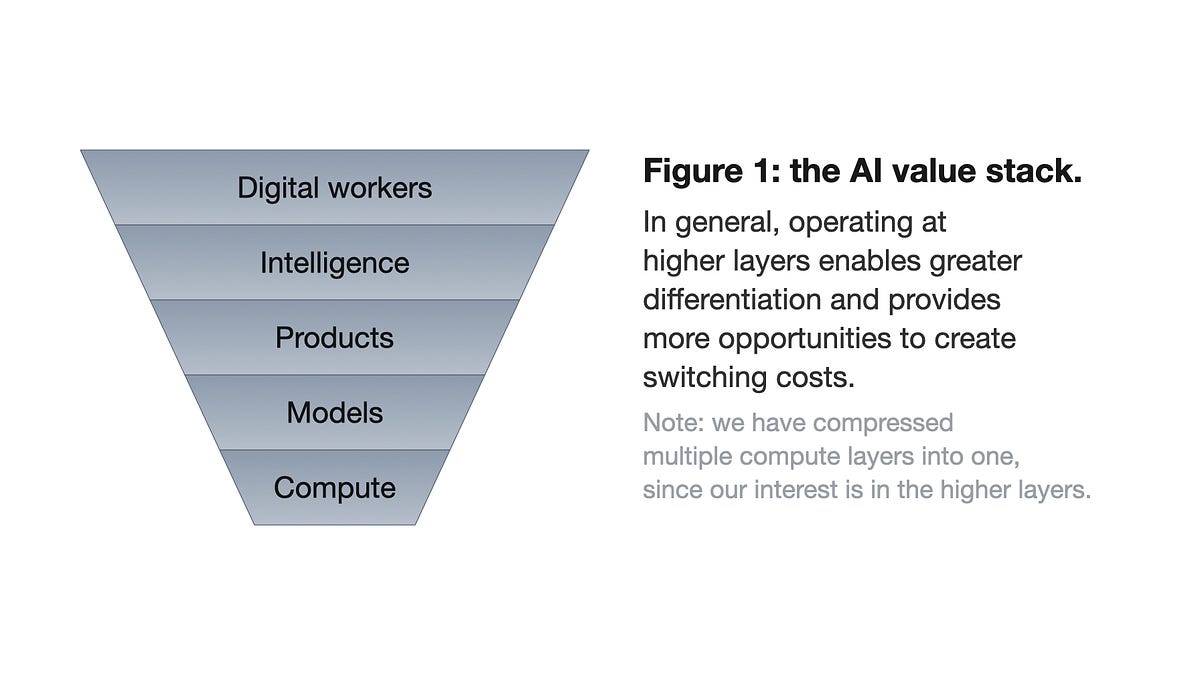

Figure 1 illustrates some of these ongoing efforts. Note that the stack describes what the customer pays for, not the billing unit. Token pricing can be used at any layer of the stack, and other units (subscriptions, outcomes) can be used in combination or as substitutes at the higher layers. It is the type of value at each layer of the stack that determines whether the commodity trap applies, not the pricing model. We discuss pricing strategies in more detail in the following section.

A key insight of this essay is that companies that operate higher in this stack can capture more of the value that they create. They can better differentiate their offerings and build a variety of moats (as we discuss below), many of which are arguably novel and more powerful than enterprise software enjoyed.

An important caveat: for AI labs, especially OpenAI and Anthropic, to move up the stack, they must compete with larger incumbents who enjoy many advantages, notably existing distribution channels and deep enterprise customer relationships. Google enjoys easy vertical integration into its existing consumer product line. SaaS incumbents, notably Microsoft, are betting that they can crack the “intelligence as a service” model faster than the AI labs can. This unevenness reshapes the competitive dynamics of the AI ecosystem, and points to important differences among the key players attempting to climb the value stack.

Moving up the stack opens up a varied and powerful set of moats

How does moving up the stack allow companies to escape the commodity trap? The answer is not simply that higher layers create more economic value. It is that they make value capturable and durable: operating higher in the stack allows labs to distinguish their offerings and to construct lock-in and switching costs of a kind unavailable to sellers of raw inference, that is, API providers. They effectively allow AI companies to escape the lack of differentiation that lies at the heart of the Bertrand paradox. Moves up the stack are not just new product strategies; they are moat-building strategies. In this section, we examine several different kinds of moats—some that labs are already building, and some that they may build in the future.

To identify what moats open up as AI companies move up from the model layer, we looked at how enterprise software companies generate pricing power and capture value, then analyzed which of those strategies are likely applicable to AI companies and what new ones become available.

We note two important nuances before we dive in. First, while moats are ways to defend market share from competitors, our interest is in analyzing AI companies’ ability to capture the value that they create for customers. Still, the strategies involved are largely the same, because both require avoiding a pricing race to the bottom.

Second, our analysis focuses on the enterprise market, since we believe that it will account for the bulk of revenues. OpenAI has pivoted in this direction recently while Anthropic has had a consistent focus on enterprise. While it is possible that ad-driven consumer products could be a significant revenue stream in the future, thereby playing a role in escaping the commodity trap, that does not undermine our thesis about enterprise moats.

1. Embedding moats: AI models are something that customers invoke in their workflows. But another vision of AI is a system that the customer inhabits. The latter is more conducive to building moats.

Even if the underlying model stays interchangeable, the state wrapped around it for a given customer may not be. Over time, that state accumulates: persistent memory and conversation history, uploaded document corpora and retrieval indexes, custom skills or evaluation suites, workflows and business processes, and various forms of fine-tuning or customization. This “data gravity” is a big part of what gives enterprise software its stickiness, and why replacing it has been described as “open-heart surgery”.

Both OpenAI (Company Knowledge) and Anthropic (Claude Cowork, the PwC partnership) are already pursuing these pathways. The durability of these strategies remains an open question. One complication is that the data that could help build moats typically sits on companies’ servers in established systems like Salesforce, Workday, and SAP, largely inaccessible to AI labs. To overcome this, AI companies could build moats by controlling the orchestration layers occupied by agents, thus effectively providing the connective tissue that binds an organization’s workflows. However, if open standards keep the orchestration layer thin and swappable, value may ultimately flow to agentic integrators and enterprises rather than the labs themselves.

2. Ecosystem moats: Enterprise software such as Windows, GitHub, and SAP all benefited from the fact that, as they gained more customers or developers that built on top of the platform, the value of the platform grew. The AI market does not yet exhibit strong ecosystem moats. Labs have made efforts to create two-sided marketplaces on top of AI as a platform, but so far these have either been unsuccessful (GPT store) or too thin to create meaningful switching costs (Claude plugins).

A much-discussed but as-yet-unrealized kind of network effect is the “flywheel” of training AI models or systems using customers’ IP, whether data, the environments in which agents execute, the execution traces of those agents, or private evaluation suites. So far, enterprises have been skittish about allowing their IP to be used this way by AI developers, but this may change in the future. After all, it takes only one (suitably incentivized) customer in each sector to defect to set a flywheel into motion.

**3. Commercial moats: **This category covers a range of familiar strategies, largely borrowed from enterprise software and cloud computing. Commercial contracts can include various mechanisms (multi-year agreements, committed-spend tiers, prepaid credits) that make defection to rivals uneconomic. The labs are already deploying some of these mechanisms in their enterprise agreements, but the durability of this moat is also questionable. Sophisticated enterprise procurement teams will demand portability before signing, and contractual lock-in is highly legible to antitrust regulators.

Vertical integration offers a more powerful version of the same commercial logic. When an AI assistant is bundled into software an enterprise already pays for (Copilot inside Microsoft 365, Gemini inside Google Workspace) the marginal cost of AI appears to be zero, making it difficult for standalone competitors to compete on price. Integrated players can also ride existing sales and procurement relationships: instead of winning a new budget line, they simply fold AI into a renewal conversation for software the customer is already committed to. Of course, this strategy is only available to integrated incumbents like Google and Microsoft. As noted above, this means that standalone labs like OpenAI or Anthropic must compete on a structurally uneven playing field, often renting infrastructure from the very companies they are up against.

4. Behavioral moats: Whereas the moats discussed above operate through technical or commercial mechanisms, behavioral moats work through the humans who use AI systems. Much like earlier waves of enterprise software (Microsoft Excel, CRM systems), the use of AI tools can lead to an erosion of the skill at performing tasks unaided, while at the same time building vendor-specific skills in driving agentic products, creating dependence. This is an area where the societal stakes may be acute, beyond its implications for value capture: skill erosion could have profound implications for workforce resilience, safety, and the distribution of power between people and AI systems.

But behavioral moats also include novel and poorly understood forms of AI lock-in that have no clean analog in earlier software. A notable manifestation is relational attachment to a model’s tone or “personality,” as vividly demonstrated by the #Keep4o backlash, when OpenAI was forced to reinstate GPT-4o in response to user demands. More speculatively, for collaborative knowledge work such as writing or judgment-heavy work (as opposed to automation), the quality of AI’s contribution is hard for the buyer to verify even after the fact, because there are no objective standards. That makes such work a so-called credence good, similar to lawyers and consultants. Unable to compare quality, buyers of credence goods tend to rely on reputation and trust. This mutes price competition and slows switching even when the technical cost of switching is close to zero.

5. Pricing strategies: This pathway is complementary or additive to the ones discussed above, and describes a way in which labs might be able to capture more value after they achieve lock-in and are able to exert pricing power. The idea is that labs may be able to overcome the commodity trap by charging for outcomes (a percentage of cost saved, a fee per resolved support ticket) rather than tokens. This is the explicit thesis behind OpenAI CFO Sarah Friar’s statement that revenue should “scale with the value of intelligence.”

However, this is unlikely in the short term. Outcome pricing requires solving a challenging measurement problem. The labs haven’t built the infrastructure to measure and understand customers’ business processes, and to track — let alone price — different outcomes. Without that visibility, outcome metrics invite gaming by both sides: a fee per resolved ticket incentivizes customers to stuff multiple issues into one ticket and vendors to close tickets without necessarily fixing them. Besides, outcomes vary between verticals and between firms, and AI labs lack the embedded customer teams that SaaS vendors spent decades building in order to gain this kind of downstream visibility. Still, some AI companies are trying to innovate on this front. If AI labs are able to migrate into Systems of Record, the challenges become tractable with enough investment.

Broader implications of the shift

The questions raised by our analysis have a significant bearing on the future of the AI economy, but they extend well beyond the prospects of any individual AI company. They touch on the structure of digital markets, the distribution of economic power, and the kind of innovation ecosystem that AI is likely to produce.

If the labs fail to escape the commodity trap, the consequences are primarily financial: a potential crisis of confidence in one of the largest capital buildouts in economic history, with ripple effects through the broader technology sector and markets in general. But if they succeed — particularly if they manage to increase switching costs and establish customer lock-in — the consequences look different, and in some ways more concerning. It would raise costs for every enterprise that depends on AI and entrench a small number of players in a position of structural advantage that will be difficult to contest later. A few questions in particular seem worth taking seriously now, before the relevant moats have hardened:

Can the labs build sustainable businesses without foreclosing competition and repeating earlier patterns of harmful concentration?

Can strategies that work for investors and AI companies also generate wider social value, or does value capture in AI come at the expense of the surrounding ecosystem?

Will the gains from AI be diffuse (accruing primarily to the enterprises that deploy it, and the broader economy) or concentrated (largely captured by hyperscalers, frontier AI labs, SaaS incumbents, and investors)?

There remains much uncertainty about these questions, but history suggests that the time to establish interoperability standards, portability requirements, and switching-cost transparency is early, before lock-in compounds and intervention becomes structurally more difficult. Fortunately, competition authorities such as the U.S. FTC and the UK CMA are watching this space, but so far they appear to have focused their analysis on the bottom layers of the stack. Our analysis shows that they must broaden their view.

We are grateful to Sayash Kapoor for feedback on a draft.

Further reading

While many aspects of our argument are at least somewhat novel, the “no moat” argument itself is not new. Its first prominent articulation (that we know of) goes back over three years, in a leaked Google document. Many commentators such as Gary Marcus, Ed Zitron, and Cory Doctorow have relentlessly made this point or variants of it. What is possibly new in our analysis is drawing from historical parallels and showing that model inference matches the prerequisites for ruinous competition even better than those precedents do. Where we definitely differ from those predicting a bubble is recognizing that (1) the AI stack is quite thick and the commodity trap only applies at the model layer (2) the labs are keenly aware of the problem and (3) have been furiously migrating their way out of it.

Many others are bearish on the labs, including Benedikt Evans and Luis Garicano and Jesús Saa-Requejo. The latter argue that *Value capture will take place both at the top of the value chain, the hardware and physical providers [because of the compute bottleneck], and in the implementation layer, where models are put to work and where the binding constraint is organizational, not technical. *We largely agree. But they conclude that the labs won’t be able to capture much value. The implicit assumption seems to be that the labs are confined to being model vendors, which in our view is an increasingly outdated notion.

Semianalysis argues that the labs will be able to sustain high gross margins because of compute scarcity. We think this is a temporary state of affairs.

Closest to our thinking is our Princeton CITP colleague Mihir Kshirsagar, who has written a series of four articles on this topic. While we have benefited from conversations with Kshirsagar, our thinking developed largely independently, with many points of agreement and some points of disagreement. Like Kshirsagar, we think the rapid AI buildout doesn’t make economic sense if it weren’t for the promise of lock-in. His analysis identifies coalitions between hyperscalers and AI labs (such as Microsoft-OpenAI and Amazon-Anthropic) as the primary vehicle for lock-in, which is slightly different from our diagnosis.

Nathan Lambert offers one vision for how this might all play out — a two-tier AI economy in which customers who are themselves at the frontier of knowledge work pay big premiums for “up the stack” products and services based on frontier models from the leading labs, while everyone else is satisfied with the open model ecosystem. One of his predictions is sharper than ours: frontier labs will let their API businesses decay in order to protect their higher-margin offerings.

1 The theoretical model behind the Bertrand Paradox is a one-shot game and switching costs don’t enter the equation, but of course in practice we must consider them.

2 This is not to say that AI will stop improving — other routes such as inference scaling and better tooling will remain.