The market treats artificial intelligence as a software phenomenon, constrained only by the supply of advanced logic chips and the electricity required to power them. But beneath the silicon and the grid lies a heavier, older physical constraint: water.

AI compute generates immense thermal density. To prevent processors from melting, that heat must be rejected into the environment, and the most efficient medium for thermal transfer is water. As a result, the AI infrastructure buildout is quietly becoming one of the largest new draws on global freshwater reserves—often in regions already facing severe structural deficits.

This is the first intersection in the Water Nexus, a cascade where the demands of the digital economy collide with the hard limits of the physical world. This is Part 1 of a four-part series on the global water chokepoint.

The Scale of the Draw #

The water footprint of modern compute is staggering, and it scales non-linearly with model complexity.

A standard hyperscale data center can consume between 1 million and 5 million gallons of freshwater per day for cooling, depending on the season and the facility’s Power Usage Effectiveness (PUE) [1]. At the micro level, UC Riverside researchers estimate that roughly 20 AI queries evaporate a 500ml bottle of freshwater [2].

Globally, the scale is staggering. Data centers consume roughly 560 billion liters of water per year, a figure projected to rise to 1,200 billion liters [3]. In the United States alone, data centers directly consumed an estimated 17.4 billion gallons of water in 2023, with an additional 211 billion gallons consumed indirectly through the thermoelectric power generation required to run them [4]. As rack densities increase from 10–15 kW to 50–100+ kW to support next-generation AI training clusters, air cooling becomes physically impossible. Liquid cooling—specifically direct-to-chip and immersion systems—becomes mandatory.

While closed-loop liquid cooling systems are highly efficient, the heat they capture must still be rejected via evaporative cooling towers, which consume massive volumes of water through evaporation and “blowdown” (flushing concentrated minerals).

The Geographic Collision #

The core problem is not just the volume of water, but where it is being drawn.

Data center siting is driven by cheap land, tax incentives, and grid interconnection availability—not hydrological abundance. Consequently, roughly two-thirds of data centers built since 2022 are located in water-stressed regions [3].

This is a global pattern, not an isolated local dispute:

United States: In Texas, data center water use is projected to surge from 49 billion gallons in 2025 to up to 399 billion gallons by 2030 [5]. In Virginia’s “Data Center Alley,” evaporative cooling is visibly depleting the Potomac basin [6].Mexico: Querétaro, the “data center capital” of Mexico, is seeing >$10B in investment while the state endures its worst drought in a century, sparking protests over water priority [7].Uruguay & Chile: Google faced intense public backlash over a planned data center in Montevideo during Uruguay’s worst drought in 74 years, and was forced to redesign a facility in Santiago, Chile, over groundwater concerns [8] [9].Ireland: Data centers now consume ~21% of national electricity, pushing the grid to the brink and forcing effective moratoriums on new connections in Dublin [6].

Compute is no longer just competing for silicon and electrons; it is competing for the fundamental resource required for human survival.

The Market Disconnect (An Honest Look) #

Despite the severity of this physical constraint, the market has largely ignored water as an investable theme. The Cascade Thesis demands an honest look at the data, not a curated narrative.

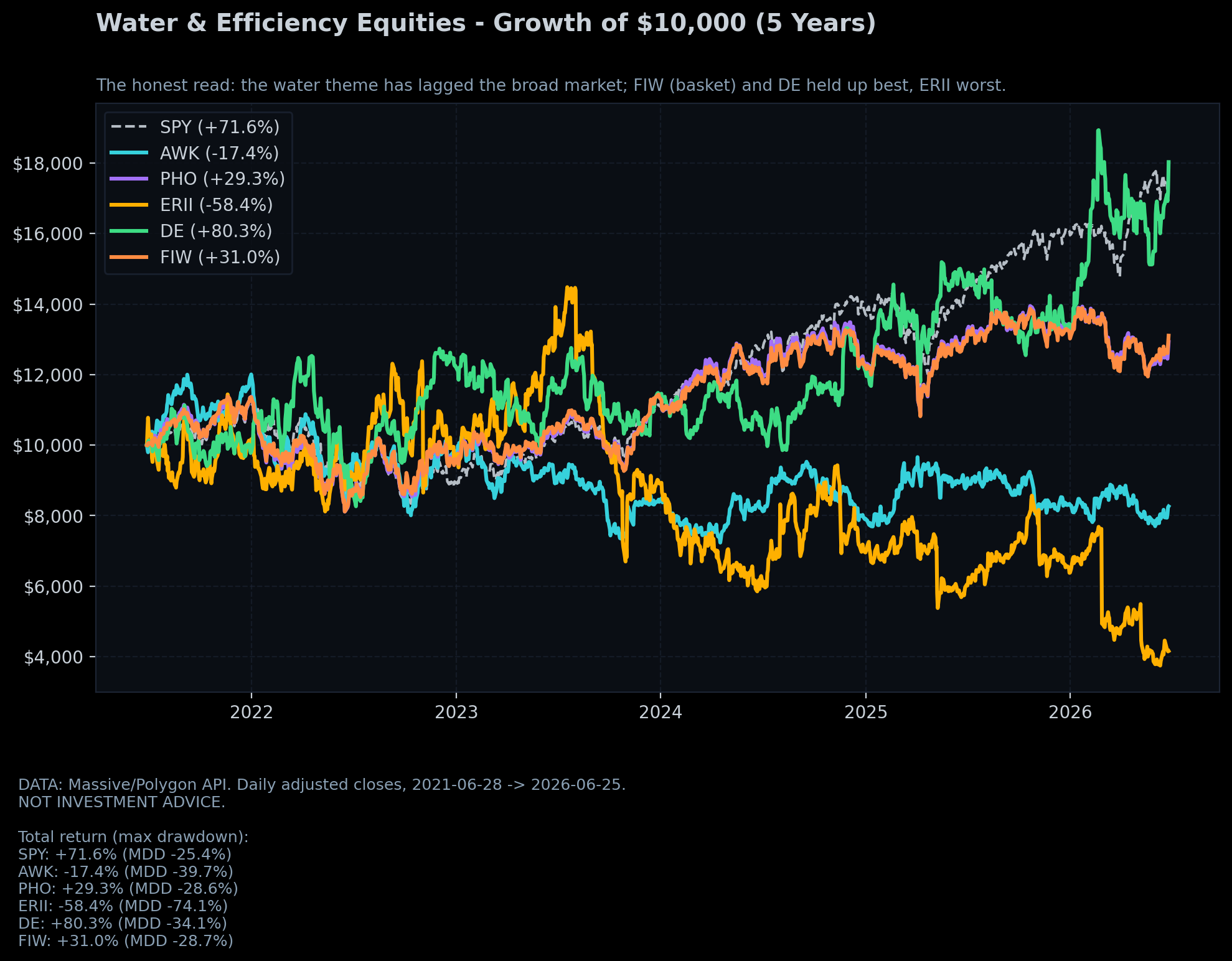

As the chart below shows, over the last five years, water equities have significantly lagged the broader market:

DATA: Massive/Polygon API. Daily adjusted closes. NOT INVESTMENT ADVICE.

While the S&P 500 (SPY) returned +71.6%, the best-performing diversified water basket, First Trust Water ETF (FIW), returned only +31.0%. American Water Works (AWK), a major regulated utility, is down -17.4%. Energy Recovery (ERII), a leader in desalination technology, suffered a brutal -74% maximum drawdown and remains deeply negative. Xylem (XYL), the large-cap water infrastructure name, returned a modest +8.3% — better than the pure-plays, but still half the market. The market is currently pricing water infrastructure as a sleepy, low-growth utility sector burdened by high interest rates and heavy capital expenditure requirements. It is entirely missing the impending demand shock from AI thermal management.

The Investable Cascade #

When an exponential demand curve (AI compute) hits an inelastic supply curve (freshwater in arid regions), the result is a repricing of the constraint. We map this through the Cascade Graph:

Cooling Infrastructure (VRT, NVT): The immediate beneficiaries are companies providing the high-density liquid cooling systems required to manage AI thermal loads. Vertiv (VRT) and nVent (NVT) are the physical tollbooths for this transition. - Water Baskets & Utilities (FIW, AWK): As permitting tightens, existing water rights and treatment infrastructure in critical data center corridors become strategic assets. The broad baskets (FIW, PHO) provide diversified exposure to this infrastructure, while regulated utilities (AWK) with the capital to build advanced reclamation facilities will command a premium. - Desalination & Water Treatment (XYL, ERII): As freshwater becomes politically toxic for data centers to consume, hyperscalers will be forced to fund zero-liquid-discharge (ZLD) systems, advanced wastewater treatment, and, in coastal regions, desalination. This is a real, growing market — but finding a clean investable expression is harder than it looks.Xylem (XYL) is the large-cap incumbent (~$30B market cap): pumps, filtration, analytics, and treatment infrastructure. It is profitable, growing, and diversified across municipal and industrial water. The risk: it is priced like a compounder (~30x earnings), and much of its revenue comes from legacy municipal contracts that have nothing to do with the AI-water collision. You are paying a premium for stability, not for the thesis.Energy Recovery (ERII) is the small-cap pure-play (~$456M market cap): they make pressure-exchanger devices that reduce the energy cost of reverse-osmosis desalination by ~60%. The technology is genuinely dominant (~90% market share in large desal). The problems are real: revenuedeclined7% in FY2025, Q1 2026 was a net loss, the stock is down ~65% from its 2021 highs, and — most concerning —insiders have been exclusively selling(14 insider trades in the last 6 months, all sales, zero purchases). The company cites Middle East project delays and lumpy contract timing. The thesis (desal becomes critical infrastructure) may be correct on a 3–10 year horizon, but the stock could easily go lower before it goes higher. This is a speculative technology bet, not a near-term catalyst play. Size accordingly or not at all.We include both so you can see the spectrum. Neither is a recommendation. Do your own work.

The thirsty machine cannot run without water. The market has priced the silicon. It has begun to price the power. It has not yet priced the coolant.

References

[1] Environmental and Energy Study Institute (EESI). “Data Centers and Water Consumption.” [2] Ren, S., et al. “Making AI Less ‘Thirsty’.” UC Riverside. [3] Bloomberg. “AI’s Thirst for Water.” May 2025. [4] AGU / Water Resources Research. “The Water Footprint of Data Centers.” [5] HARC / University of Houston study. [6] Lincoln Institute of Land Policy. “Land and Water Impacts of Data Centers.” Oct 2025. [7] BBC News. “Mexico’s data centre boom.” Aug 2025. [8] Logic Magazine / Mongabay. “Google’s Uruguay Data Center.” [9] Mongabay / DW. “Chile data center redesign.”

Found this useful? AtomProphet is independent and reader-funded — you can support the research & hosting ↓

Get the next cascade in your inbox

One short email when a new analysis drops — a single constraint traced end to end, from the physics to the chokepoint to the tickers, with the honest bear case kept in view. No marketing, no tracking, no noise.

- One email per published analysis — typically a few a month, never a daily blast

- The full cascade: driver → chokepoint → vetted, live-liquidity tickers

- The counter-case spelled out, not buried

No account, no paywall. Double opt-in, and one-click unsubscribe in every email.

Support the research & hosting

AtomProphet is independent, ad-light, and reader-funded. Contributions help cover data feeds, hosting, and the time behind the Cascade Graph — they keep this research free and open. A tip buys nothing, unlocks nothing, and is not payment for advice or for any security mentioned anywhere on this site.

Bitcoin37h98hpiHz6BW6ELvRLagk7BBo8UUtxeSh

USDC · Base 0x1ac1Abe9eCAd5fAd8fF55B188E079b52cD1e6415