It might be simpler than you think. Etched, Fractile, MatX, Positron, Rebellions, SambaNova, Tensordyne, Tenstorrent, and more.

Two AI chip startups had huge financial outcomes in the past year. Groq was acquired for $20B, and Cerebras IPO’d to a $40B+ market cap. Huge, but not trillion-dollar huge. And in this environment, an inference-first system that runs frontier models and scales to gigawatts of compute has a real shot at a trillion-dollar market cap if it can scale, grow, and IPO.

But Groq and Cerebras run architectures you can poke holes in. Both were designed before LLMs went mainstream, and their early design choices don’t suit today’s models. I call them “preGPT” accelerators.

The famous example (well-covered ground already) is that they’re SRAM-only. It takes many Groq racks to serve even one smallish model, and even Cerebras’ wafer-scale marvel (900,000 cores on one piece of silicon) can’t hold a frontier model’s weights on a single wafer, so you have to expand to many wafer-level systems. Tough economics, a KV cache that doesn’t scale gracefully, and so on.

Admittedly, I looked at these engineering details and figured these companies were dead in the water when it came to LLMs. Well, to their credit, who could have predicted such thicc models 10 years ago? But no HBM to support long-context... how will they survive? More context is better…. failure to thrive?

What’s important is that they both had production silicon available, and, regardless of the shortcomings of SRAM-only architecture, they outperformed GPUs on a certain KPI (interactivity). As Jensen nicely drew for us, SRAM chips for decode unlocked new possibilities on the Pareto frontier for 2026:

And that’s why they had eleven figure outcomes. *$XX Billion, kind of nuts right! *

I was so wrong about architectural shortcomings preventing success.

Looking back, what mattered most? Timing.

Groq was in production right when Nvidia came calling. Cerebras, right when OpenAI did. Forget the architectural shortcomings. If you can ship and unlock a new Pareto frontier, good things happen. In fact, I thought the fundamental problem for Groq and Cerebras was being too early, making design decisions before transformers took off. Being too early is indistinguishable from being wrong...

And yes, starting that early nearly killed them; both came close to running out of cash. But starting early was also the whole advantage, because when the unforeseen inference wave hit, they had silicon in production. Well, they were both still default dead until Meta released Llama, the first useful open weights LLM, which allowed Groq to go show the world how awesome a super fast chatbot experience was.

Again, the combination of production silicon at the right moment and a Pareto frontier the GPU can’t reach is all that mattered. And then Nvidia’s Dynamo was icing on the cake, disaggregating the workload so the memory-bound decode could run on SRAM chips.

The postGPT era #

If the first era of inference was GPUs, Groq and Nvidia ushered in the next era with the GPU+LPU inference. But another era is incoming. The postGPT accelerators. Rack-scale systems specifically designed for LLM inference from day one. From matmuls to interconnects to memory hierarchy. There are many startups in this space, not to mention custom silicon XPUs (Maia, MTIA, Trainium, etc). So which of these could be the next Groq/Cerebras with a whale of a customer and an acquisition/IPO?

What it takes to be the next trillion-dollar chip company #

If we’ve learned anything so far, it’s that we shouldn’t overindex on engineering architectures. Sure they matter in the long run, but in this demand environment, contenders simply need to hit these four criteria: Runs frontier 1T+ modelsShips rack-scaleBeats the incumbent on one KPI****Lands a frontier anchor

Runs frontier 1T+ models. Frontier models are where the value gets captured and where scale happens, so frontier customers are the ones most willing and incentivized to deploy a postGPT accelerator at volume. A system that can’t run a 1T-param model is playing a sub-frontier game. I’m bullish on the usefulness of sub-frontier, especially in the enterprise, but the SAM is small. They won’t mint the next Groq/Cerebras.

Ships rack-scale. The race to gigawatt-scale inference runs on racks. To win, one must design and deploy racks of accelerators, quickly and reliably.

Beats the incumbent, clearly, on one KPI. The challenger doesn’t need to be best at everything. But they must be an order of magnitude better at something.

Lands a frontier anchor. The challenger needs someone serious about gigawatt-scale and buying into a roadmap and building a long-term relationship. A model lab or hyperscaler is best. Could be a big neocloud. Probably not a sovereign.

Of course, software support is table stakes.

But otherwise, I think it’s that simple.

Yes, the technical details matter; quantization, memory hierarchy, scale-up domain size, etc. But truly, right now they matter only insofar as they lead to differentiated performance (”beats the incumbent on one KPI”). The architecture behind each contender is in the teardowns; up here, judge them by the KPI it buys.

This is a unique time. Token demand FAR exceeds supply, and the shortage is worst for low-latency frontier tokens, where GPUs can’t keep up or can only do so at uneconomical throughput. This high-interactivity token scarcity turned “good enough architecture in production” into a winning hand for Groq and Cerebras.

But it’s time-bound; there was a window, and Groq/Cerebras grabbed it. And being first matters.

Which raises the next question: what’s the next window, and who will get there soonest?

Picking the next winner could be as simple as asking who can deploy a gigawatt of postGPT inference accelerators soonest?

To answer that, here’s the rest of the piece.

The frontier race, all eleven ranked by when their frontier rack ships, as a scoreboard and a timeline** A full teardown of Tenstorrent**, the only one serving a frontier-class rack today, a free sample of the diligence[Paid]

The other ten teardowns, each scored and sourced, the frontier contenders, the decode add-in, and the sub-frontier plays[Paid]

The receipts, only two of the eight frontier names have a clean third-party number[Paid]

Who actually looks like the next trillion-dollar chip company, and the argument that reframes the whole list

The frontier race: who reaches rack-scale, soonest #

Well then: “Which startups clear those four hurdles, sorted by ship date soonest?”

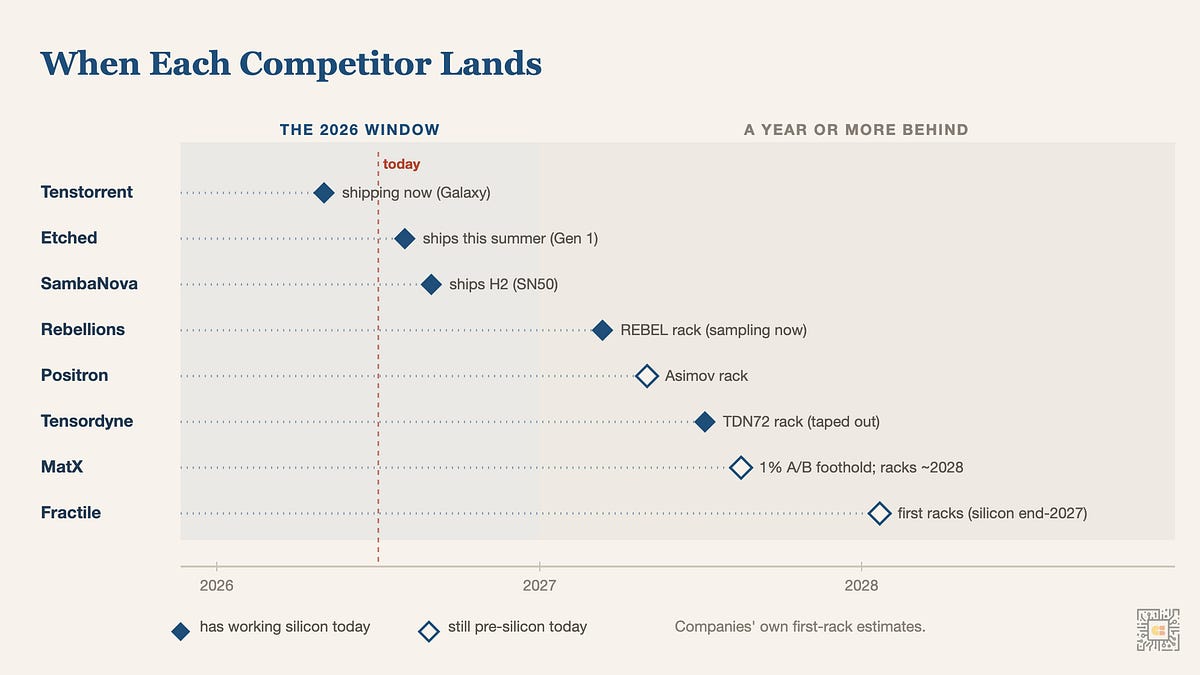

Let’s take a look. I’ve sorted them by when they claim their frontier-class generation hits rack scale. Take it with a grain of salt, and remember this isn’t yet anything about performance, but just when they say they’ll have silicon deployed.

Also note that many of these companies have shipped products already, but the earlier products were sub-frontier as they pivoted their way toward rack scale for modern frontier LLMs. So I’m only focusing on when they are shipping frontier-capable products according to their roadmap

If we scour all the public sources (press releases, blogs, podcasts), we get the following: Visualized:

Caveat though. Every entry above is a first-rack or first-sample milestone, not a gigawatt figure. IMO first rack matters, but time to first gigawatt matters most.

First rack proves the whole shebang works. But gigawatt scale proves the company works.

Who is shipping in 2026, and who isn’t?

Tenstorrent, Etched, and SambaNova ship production racks in 2026.

A year back sit Positron, Tensordyne, and Rebellions. Rebellions claims 2026, but its frontier REBEL is still only sampling, so its real rack is more like 2027.

Fractile and MatX are two years back. Both have 2027 milestones on their roadmaps, but those are samples and footholds, not scaled production shipments. Production racks at customers are realistically a 2028 story.

In this supply-starved environment, a year is expensive. That’s not to say the 2027+ companies aren’t technically competitive, nor does it imply they won’t win serious customer share in the grand arc of time. After all, it only takes one of the few large customers to get to scale. But you’re not in the game until you’re on the field! No matter how technically sound your architecture is, if you’re not on the field, you’re not in the game.

Who will be on the field first?

Tenstorrent claims to be “shipping production silicon now”. Promising! But what about customers? Tenstorrent has neoclouds and sovereigns; no frontier lab or hyperscaler has been announced yet. Could those early customers accelerate Tenstorrent to gigawatt scale? We dig into that in its teardown below.

An acquisition could help Tenstorrent get to market, as big silicon incumbents already have relationships with hyperscalers. Qualcomm was reported in mid-June to be circling a roughly $8–10B deal. But Keller supposedly denied any Qualcomm talks recently, so that path looks cold for now.

Etched is a bigger contender than it looked just months ago. It claims rack-scale shipments this summer, well ahead of the other popular names like MatX and Fractile. I think Etched was left for dead, but it turns out they are alive and claim to be right at the front of the line.

Notably, Etched is talking gigawatts. It claims “a path to gigawatt-scale in 2027,” and it’s talking about building the company infrastructure to pull it off with a Taiwan factory, plus a data center, test house, and NPI prototyping lab at its San Jose HQ. From the press release, co-founder Rob Wachen said “Our approach from the beginning has been to build for gigawatt-scale... Production is the product.”

Etched hasn’t disclosed specific customers but mentioned $1B+ in contracts booked. Etched’s talk about a “path to gigawatt-scale” and “building for gigawatt-scale” seems to imply they are targeting the type of companies that can support that scale.

Whether Etched actually hits gigawatt scale in 2027 remains to be seen, but it’s at least aimed at the right target if they want to be in the trillion-dollar race.

SambaNova also claims a 2026 deployment on its frontier SN50 landing in the second half. *This is going to make for an exciting 2H26 and early 2027 if we’ve got SambaNova, Etched, and Tenstorrent all shipping competitive racks! *

So far, SambaNova’s named customers are enterprises JPMorgan Chase and SoftBank, and these are explicitly NOT gigawatt installations. From Sally Ward-Foxton

SambaNova has a multi-year agreement in place with JPMorganChase.

“This is a breakthrough because most suppliers haven’t figured out how to get into the enterprise,” Liang said. “The enterprise market is going to be significant; it won’t be 100%, but it’s going to be a meaningful player in the overall market, and we’re starting to see that.”

Enterprise customers are looking to host private models and private data in their own environment,

which is unlikely to be a gigawatt-scale data center, Liang said.

Of course, if you have tens of 50-100MW deployments, well, that counts!

Maybe SambaNova’s plan is to demonstrate feasibility with reasonably sized enterprises and use that success to try to win hyperscalers? Or just win with enterprises, which should turn into a very large market on its own.

Behind the 2026 crew are five more competitors including Rebellions, Positron, and Tensordyne in 2027, with Fractile and MatX not reaching production racks until 2028.

Rebellions reaches a rack soonest of this 2027+ tier, with REBEL sampling now. But its named customers, mostly Korean enterprises plus Saudi Aramco, sit on the sub-frontier ATOM, not the frontier REBEL, and none is a gigawatt buyer.

Positron has a promising customer, Oracle.

Some consider OCI (Oracle Cloud Infrastructure) a hyperscaler and others call it a neocloud (* ClusterMax rates it as a gold tier neocloud*). Regardless, OCI can support GW scale installations.

So is a promising path to GW scale for Positron, and they are the first on this list who can publicly say they’re already deployed in a hyperscaler. The catch is that Oracle is currently running Atlas, Positron’s sub-frontier first-gen server. It’s not rackscale. The frontier system, Asimov, doesn’t tape out until late 2026.

So Positron already has a customer who could scale to a gigawatt, just not yet on a frontier product.

Tensordyne recently announced its Napier system has been taped out on TSMC 3nm and production is underway. And Tensordyne’s logarithmic math approach is super interesting.

But its customer book looks a lot like Tenstorrent’s. Cirrascale and BlueSky Compute are named, plus a dozen-plus letters of intent to evaluate beta systems, and roughly $200M of forecast, not booked, demand. Real interest, but neoclouds and LOIs, not a frontier lab ordering a gigawatt.

Fractile is further out. Its roadmap targets a late-2026 commercial tape-out, customer samples in Q2 2027, and production silicon only at the very end of 2027, so racks in customer data centers are realistically a 2028 story. But it’s courting exactly the right customer. In May 2026, The Information reported Anthropic was in early talks to buy Fractile chips once they ship, which would make a frontier lab its anchor, the kind that scales fastest. The talks were preliminary and the deal size wasn’t disclosed* *though.

MatX is pre-silicon, on roughly the same clock as Fractile. It targets tape-out within a year of its $500M Feb 2026 raise, first chips a few months after that, and a 2027 foothold inside a frontier lab, routing ~1% of production traffic to its silicon as an A/B test.

That foothold is a validation experiment, not production racks; by Pope’s own tape-out-to-production math of one to two years, volume racks are a 2028-at-earliest story.

It hasn’t dated real rack scale, only that CEO Reiner Pope “would like to be... shipping multiple gigawatts a year” (Cheeky Pint). So it’s got the right goal, just behind on the timeline.

Yet it may have the best customer list of anyone here. MatX says it sells only to frontier labs, “maybe five different customers in the world” and its 1% trial would be a foothold with such a customer. If that little trial is a success, that’s the type of customer who would scale quickly to a gigawatt faster than any neocloud or enterprise mentioned.

Deeper Teardown #

Of course, details matter. Here’s the due diligence on eleven companies with one question for each.

Can it put a frontier-class rack in front of a whale of a customer before the window closes?

Below is the summarized diligence on all eleven, the eight frontier contenders first, then the add-in and the sub-frontier plays.

For each we’ll hit on KPI is the one outcome the chip beats a GPU on.Anchor is who is actually deploying it.Architecture****Verified?

Then a bunch of extra sourced details.

Tenstorrent (Q2 2026)

Jim Keller is arguing a contrarian narrative. One chip runs everything, no disaggregation. Keller believes that, in the long run, general-purpose can perform as well as specialized + disaggregation.

KPI: low cost at high interactivity. Runs ~any model (~90% of Hugging Face), prefill and decode on the same silicon.Anchor: five-plus neocloud colos serving live, plus sovereign and IP licensing (Japan, LG).*No frontier lab, no hyperscaler.*Architecture: GDDR6, no HBM; RISC-V Tensix cores; Ethernet scale-out on-chip; 100% open-source software stack. One chip runs both prefill and decode, the deliberate counter to disaggregation.**Verified?**⚠️ DeepSeek ~308 tok/s/user is a served-model number, but relayed by Keller, not an independently-published AA figure. The Prodia video claim is similar: AA independently ranks Prodia’s model at the top of its leaderboard, but that predates the Tenstorrent partnership, and the 10× speed-on-Tenstorrent-hardware number is Tenstorrent/Prodia’s own benchmark, not AA-reproduced. No MLPerf; the 350→500 tok/s headline is partly forward-looking.

DETAILS

The anti-thesis, on record.

At TT-Deploy (May 2026), Jim Keller bet against specialization and disaggregation:

*“the big fad is disaggregation, special purpose hardware, SRAM. Do you know how many people are going to be talking about that in 2 years? None.”*And:

*“you don’t just run part of an LLM… that’s not a good business plan long run. You could be one-shotted by one model.”*Stan Sokorac’s (Sr. Fellow, Software) proof point: a pipeline that downloads random Hugging Face models achieves a

~90% pass rate, so*“we can run ~2.5M of the 2.8M models on Hugging Face.”*(TT-Deploy keynote;Sokorac talk)

Architecture.

Tensix core= matrix engine + vector unit + 5 “baby” RISC-V cores per tile, each with local L1 SRAM, over a 2D NoC mesh (no shared global memory); Blackhole adds16 “big” 64-bit RISC-V CPU cores and can run host-less (The Register).Anti-disaggregation by design: each chip has SRAM + DRAM + networking, so it runs prefill + decode + video on the same silicon (Vasiljevic talk).Scale-out: standard Ethernet,10×400 Gbps = 1 TB/s chip-to-chip, the anti-NVLink bet. Blackhole = TSMC 6nm.** Memory:large on-chip SRAM + GDDR6, explicitly no HBM. Official Blackhole spec: 180 MBon-chip SRAM, 28–32 GB GDDR6 at 448–512 GB/s**(tenstorrent.com/hardware/blackhole).

Shipping status.

Three taped-out generations (Grayskull → Wormhole → Blackhole).

Shipping Blackhole cards:

120 Tensix / 664 TFLOPS BLOCKFP8 / 300 W; p100a**$999**, p150a/b**$1,399**.Blackhole

Galaxy production servers reached GA Apr 28 2026(6U, 32 chips, 23 PFLOPS dense FP8,~$110K) (The Register GA).Yield caveat, now in the official spec: launched at 140 Tensix, a

Jan 2026 firmware cut to 120(≈1–2% perf hit on typical workloads; new cards ship Bin-3 parts with two disabled Tensix columns) (Tom’s Hardware).“Installed in

≥5 neocloud colos outside Tenstorrent” goal hit (TT-Deploy).

Deployments / anchors.

Infra/colo/neocloud + finance, not hyperscalers:

Equinix, Cirrascale, ai&, Prodia Labs, Virtu Financial, Turiyam, OrionVM(Tenstorrent newsroom).The other half is RISC-V/chiplet IP licensing + sovereign design:

Japan/LSTC(Ascalon IP, Rapidus), a**~$50M** Japan program to train 200 designers,LG co-developing SoCs.The gigawatt question. The July 2026 slate widened the book (Galaxy superclusters now anchorEquinix’s Distributed AI Hub, launched with OrionVM and BetterBrain, plus new ai&, Virtu Financial, and Cirrascale deployments), but none of it is gigawatt-class. The headline neocloud, Cirrascale, isClusterMAX Silver, running in the thousands of GPUs, and already lost OpenAI to Azure (ClusterMAX). Every name here buys racks, yes, but not gigawatts. Aggregating many mid-size buyers may get there, but slower.

Performance / verification.

Absent from MLPerf v6.0.

~308 tok/s/user on DeepSeek live is a served-model measurement, but per Keller’s own telling, not an independently published Artificial Analysis number; the roadmap to500 tok/s/user at $6/M TCO is forward-looking.The

Prodia video record(Wan 2.2, 2.4s, 10× a GPU) needs the same unpacking: Prodia’s model already led the Artificial Analysis leaderboardbeforethe Tenstorrent partnership, so that ranking is genuinely AA-verified — but the10× speedup on Tenstorrent hardware(33.8 fps vs. 5.5 fps on Nvidia) is Tenstorrent and Prodia’s own collaboration benchmark, not a number AA independently re-ran (Tenstorrent newsroom;Vasiljevic talk).Stack is

100% open source(TT-Forge, TT-Lang), the anti-CUDA-moat argument. Team / funding.

Founded

2016(Toronto) by Ljubisa Bajic, Ivan Hamer, and Milos Trajkovic;** Jim KellerCEO since ~2023. Series D $693M+closed Dec 2024 at~$2.6–2.7B post**(Samsung Securities + AFW lead; Bezos, Hyundai, LG) (Series D).A reported

~$800M / ~$3.2B Fidelity round (Nov 2025) is not company-confirmed.

That’s the free read. Behind the paywall:

The other ten teardowns, each scored on the same four questions as Tenstorrent, its KPI, its anchor, its architecture, and what’s actually verified, then the full sourced details behind every line. The seven remaining frontier contenders (Etched, Rebellions, SambaNova, Positron, Tensordyne, Fractile, MatX), the decode add-in (d-Matrix), and the two sub-frontier plays (Furiosa, Taalas).The verification scorecard, which two of the eight frontier contenders have a clean independent number, which one has only a partner-run result, and which remain vendor-stated.Which “frontier” chips can’t yet run a frontier model, the sub-1T ceiling sitting under every verified number, and whose only MLPerf result is for the wrong chip.The memory split, company by company, who leans on HBM for raw bandwidth and who drops it for commodity LPDDR or GDDR to dodge the supply crunch, and what each choice costs them.Where the field lands on disaggregation, one chip running prefill and decode versus a split tier, and which way it’s converging.Who actually looks like the next trillion-dollar chip company, and the specialization argument, Jim Keller against Gavin Uberti, that frames the whole list.

If you’re deciding who to watch, partner with, invest in, or compete against, this is the half that matters.

### Etched (H2 2026)

A frontier inference system, sold as a full rack, has its real edge in low-voltage inference and cluster-scale memory. And more flexible than it’s remembered for: the system that launched in June runs DeepSeek, Qwen, Llama, and Mamba. Mamba is an SSM, not a transformer… *so clearly it’s more flexible than previous talk of “transformer-only ASIC” made it out to be… *